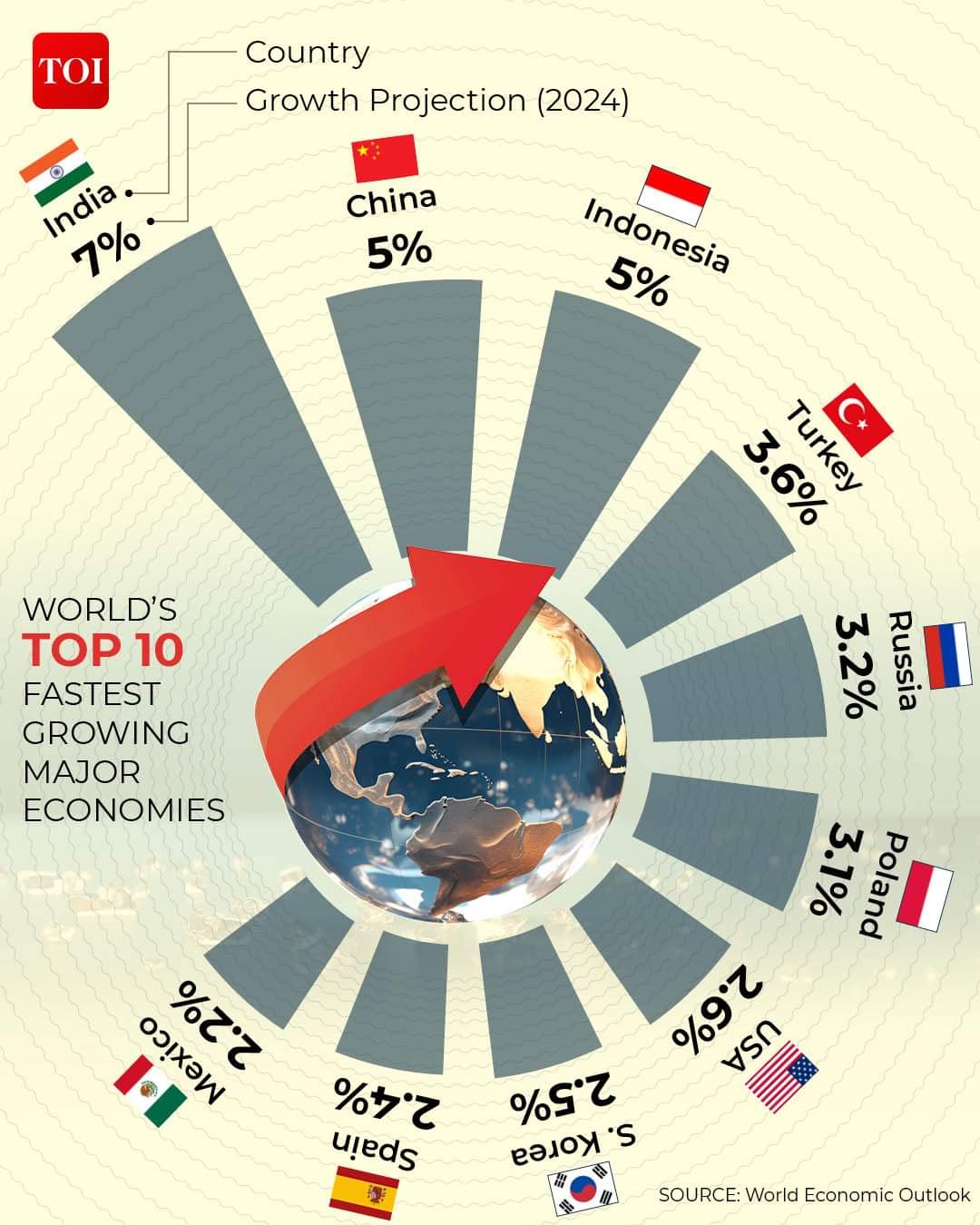

In a significant milestone for the global economy, India has overtaken both the United States and China to emerge as the fastest-growing major economy in the world in 2024. The International Monetary Fund (IMF) has projected that India’s economy will grow at an impressive rate of 7% this year, with further growth of 6.5% expected in 2025. This marks a pivotal moment for India, as it solidifies its position as a leading economic power on the world stage.

Economic Resilience Amid Global Uncertainty

India’s rapid economic expansion comes amid a backdrop of global economic uncertainty. While many developed and emerging economies have been grappling with the lingering effects of the COVID-19 pandemic, supply chain disruptions, and geopolitical tensions, India has managed to navigate these challenges with remarkable resilience. The IMF attributes India’s robust growth to a combination of factors, including strong domestic demand, a burgeoning technology sector, and government initiatives aimed at bolstering infrastructure and manufacturing.

India’s growth rate stands in stark contrast to the projections for other major economies. The IMF has forecasted that the U.S. economy will grow by 2.3% in 2024, while China’s growth is expected to slow to 4.8% as the country faces structural economic challenges and demographic shifts. This divergence in growth rates underscores India’s emergence as a key driver of global economic activity.

Key Drivers of Growth

Several factors have contributed to India’s remarkable economic performance:

- Technological Innovation: India’s technology sector has been a significant engine of growth, with the country continuing to lead in software services, digital payments, and fintech innovations. The proliferation of startups and the rise of unicorns have further fueled economic activity and job creation.

- Infrastructure Development: The Indian government has prioritized infrastructure development, launching ambitious projects to modernize transportation, energy, and urban infrastructure. These initiatives have not only created jobs but also improved connectivity and efficiency, attracting both domestic and foreign investment.

- Manufacturing and Exports: India’s focus on boosting its manufacturing capabilities, particularly through the “Make in India” initiative, has started to pay off. The country has seen a surge in exports of electronics, automobiles, and pharmaceuticals, contributing to economic growth and reducing its reliance on imports.

- Rural Economy and Agriculture: The rural economy, bolstered by favorable monsoons and government support for agriculture, has also played a crucial role in driving growth. Increased agricultural productivity and higher rural incomes have led to a rise in consumption and demand for goods and services.

Challenges and the Road Ahead

Despite the impressive growth figures, India faces several challenges that could impact its long-term economic trajectory. Income inequality, job creation in non-agricultural sectors, and the need for significant reforms in education and healthcare remain pressing issues. Additionally, global economic conditions, such as fluctuations in energy prices and trade tensions, could pose risks to sustained growth.

Nevertheless, India’s economic outlook remains positive. The government’s continued focus on reforms, digitalization, and infrastructure development is expected to sustain momentum in the coming years. With a young and dynamic population, India is well-positioned to maintain its status as the fastest-growing major economy and contribute significantly to global economic growth.

As India enters this new phase of economic ascendancy, it is poised to play an increasingly influential role on the global stage, shaping the future of trade, technology, and sustainable development. The world will be watching closely as India continues its journey towards becoming an economic superpower.